Joseph Stiglitz couldn’t believe his ears. Here they were in the White House, with President Bill Clinton asking the chiefs of the US Treasury for guidance on the life and death of America’s economy, when the Deputy Secretary of the Treasury Larry Summers turns to his boss, Secretary Robert Rubin, and says, “What would Goldman think of that?”

Joseph Stiglitz couldn’t believe his ears. Here they were in the White House, with President Bill Clinton asking the chiefs of the US Treasury for guidance on the life and death of America’s economy, when the Deputy Secretary of the Treasury Larry Summers turns to his boss, Secretary Robert Rubin, and says, “What would Goldman think of that?”

The tsunami of populist rage coursing through America is bigger than Daschle’s overdue tax bill, bigger than John Thain’s trash can, bigger than any bailed-out C.E.O.’s bonus. It’s even bigger than the Obama phenomenon itself. It could maim the president’s best-laid plans and what remains of our economy if he doesn’t get in front of the mounting public anger.

Larry Summers: Goldman Sacked September 17, 2013

Posted by rogerhollander in Barack Obama, Economic Crisis.Tags: bail out, cfma, deregulation, derivitives, Economic Crisis, Federal Reserve, foreclosures, Goldman Sachs, Greg Palast, jon corzine, Larry Summers, lending club, robert rubin, roger hollander, stiglitz, sub-prime mortgage, the fed, Wall Street

add a comment

|

|||||||||||||||

Secrets and Lies of the Wall Street Bailout January 9, 2013

Posted by rogerhollander in Economic Crisis.Tags: bailout, bank of america, citigroup, Economic Crisis, Federal Reserve, financial crisis, Goldman Sachs, hamp, Hank Paulson, Larry Summers, matt taibbi, Morgan Stanley, roger hollander, tarp, the fed, tim geithner, timothy geithner, Wall Street

add a comment

Roger’s note: One does not have to have a Ph.D. in Economics to understand the words “lies” and “secrets.” Matt Taibbi is one of the finest journalists writing today, and he painstakingly outlines the fraud perpetuated on the American people by the Republicrat government in collusion with the Wall Street financial institutions.

Published on Tuesday, January 8, 2013 by Rolling Stone

The federal rescue of Wall Street didn’t fix the economy – it created a permanent bailout state based on a Ponzi-like confidence scheme. And the worst may be yet to come

by Matt Taibbi

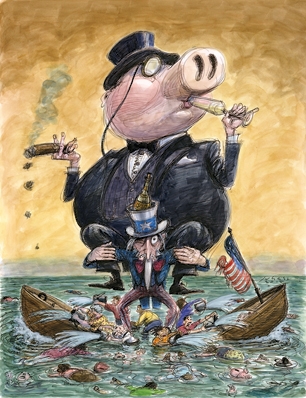

It has been four long winters since the federal government, in the hulking, shaven-skulled, Alien Nation-esque form of then-Treasury Secretary Hank Paulson, committed $700 billion in taxpayer money to rescue Wall Street from its own chicanery and greed. To listen to the bankers and their allies in Washington tell it, you’d think the bailout was the best thing to hit the American economy since the invention of the assembly line. Not only did it prevent another Great Depression, we’ve been told, but the money has all been paid back, and the government even made a profit. No harm, no foul – right?

(Illustration by Victor Juhasz)

Wrong.

It was all a lie – one of the biggest and most elaborate falsehoods ever sold to the American people. We were told that the taxpayer was stepping in – only temporarily, mind you – to prop up the economy and save the world from financial catastrophe. What we actually ended up doing was the exact opposite: committing American taxpayers to permanent, blind support of an ungovernable, unregulatable, hyperconcentrated new financial system that exacerbates the greed and inequality that caused the crash, and forces Wall Street banks like Goldman Sachs and Citigroup to increase risk rather than reduce it. The result is one of those deals where one wrong decision early on blossoms into a lush nightmare of unintended consequences. We thought we were just letting a friend crash at the house for a few days; we ended up with a family of hillbillies who moved in forever, sleeping nine to a bed and building a meth lab on the front lawn.

How Wall Street Killed Financial Reform

But the most appalling part is the lying. The public has been lied to so shamelessly and so often in the course of the past four years that the failure to tell the truth to the general populace has become a kind of baked-in, official feature of the financial rescue. Money wasn’t the only thing the government gave Wall Street – it also conferred the right to hide the truth from the rest of us. And it was all done in the name of helping regular people and creating jobs. “It is,” says former bailout Inspector General Neil Barofsky, “the ultimate bait-and-switch.”

The bailout deceptions came early, late and in between. There were lies told in the first moments of their inception, and others still being told four years later. The lies, in fact, were the most important mechanisms of the bailout. The only reason investors haven’t run screaming from an obviously corrupt financial marketplace is because the government has gone to such extraordinary lengths to sell the narrative that the problems of 2008 have been fixed. Investors may not actually believe the lie, but they are impressed by how totally committed the government has been, from the very beginning, to selling it.

They Lied to Pass the Bailout

Today what few remember about the bailouts is that we had to approve them. It wasn’t like Paulson could just go out and unilaterally commit trillions of public dollars to rescue Goldman Sachs and Citigroup from their own stupidity and bad management (although the government ended up doing just that, later on). Much as with a declaration of war, a similarly extreme and expensive commitment of public resources, Paulson needed at least a film of congressional approval. And much like the Iraq War resolution, which was only secured after George W. Bush ludicrously warned that Saddam was planning to send drones to spray poison over New York City, the bailouts were pushed through Congress with a series of threats and promises that ranged from the merely ridiculous to the outright deceptive. At one meeting to discuss the original bailout bill – at 11 a.m. on September 18th, 2008 – Paulson actually told members of Congress that $5.5 trillion in wealth would disappear by 2 p.m. that day unless the government took immediate action, and that the world economy would collapse “within 24 hours.”

To be fair, Paulson started out by trying to tell the truth in his own ham-headed, narcissistic way. His first TARP proposal was a three-page absurdity pulled straight from a Beavis and Butt-Head episode – it was basically Paulson saying, “Can you, like, give me some money?” Sen. Sherrod Brown, a Democrat from Ohio, remembers a call with Paulson and Federal Reserve chairman Ben Bernanke. “We need $700 billion,” they told Brown, “and we need it in three days.” What’s more, the plan stipulated, Paulson could spend the money however he pleased, without review “by any court of law or any administrative agency.”

The White House and leaders of both parties actually agreed to this preposterous document, but it died in the House when 95 Democrats lined up against it. For an all-too-rare moment during the Bush administration, something resembling sanity prevailed in Washington.

So Paulson came up with a more convincing lie. On paper, the Emergency Economic Stabilization Act of 2008 was simple: Treasury would buy $700 billion of troubled mortgages from the banks and then modify them to help struggling homeowners. Section 109 of the act, in fact, specifically empowered the Treasury secretary to “facilitate loan modifications to prevent avoidable foreclosures.” With that promise on the table, wary Democrats finally approved the bailout on October 3rd, 2008. “That provision,” says Barofsky, “is what got the bill passed.”

But within days of passage, the Fed and the Treasury unilaterally decided to abandon the planned purchase of toxic assets in favor of direct injections of billions in cash into companies like Goldman and Citigroup. Overnight, Section 109 was unceremoniously ditched, and what was pitched as a bailout of both banks and homeowners instantly became a bank-only operation – marking the first in a long series of moves in which bailout officials either casually ignored or openly defied their own promises with regard to TARP.

Congress was furious. “We’ve been lied to,” fumed Rep. David Scott, a Democrat from Georgia. Rep. Elijah Cummings, a Democrat from Maryland, raged at transparently douchey TARP administrator (and Goldman banker) Neel Kashkari, calling him a “chump” for the banks. And the anger was bipartisan: Republican senators David Vitter of Louisiana and James Inhofe of Oklahoma were so mad about the unilateral changes and lack of oversight that they sponsored a bill in January 2009 to cancel the remaining $350 billion of TARP.

So what did bailout officials do? They put together a proposal full of even bigger deceptions to get it past Congress a second time. That process began almost exactly four years ago – on January 12th and 15th, 2009 – when Larry Summers, the senior economic adviser to President-elect Barack Obama, sent a pair of letters to Congress. The pudgy, stubbyfingered former World Bank economist, who had been forced out as Harvard president for suggesting that women lack a natural aptitude for math and science, begged legislators to reject Vitter’s bill and leave TARP alone.

In the letters, Summers laid out a five-point plan in which the bailout was pitched as a kind of giant populist program to help ordinary Americans. Obama, Summers vowed, would use the money to stimulate bank lending to put people back to work. He even went so far as to say that banks would be denied funding unless they agreed to “increase lending above baseline levels.” He promised that “tough and transparent conditions” would be imposed on bailout recipients, who would not be allowed to use bailout funds toward “enriching shareholders or executives.” As in the original TARP bill, he pledged that bailout money would be used to aid homeowners in foreclosure. And lastly, he promised that the bailouts would be temporary – with a “plan for exit of government intervention” implemented “as quickly as possible.”

The reassurances worked. Once again, TARP survived in Congress – and once again, the bailouts were greenlighted with the aid of Democrats who fell for the old “it’ll help ordinary people” sales pitch. “I feel like they’ve given me a lot of commitment on the housing front,” explained Sen. Mark Begich, a Democrat from Alaska.

But in the end, almost nothing Summers promised actually materialized. A small slice of TARP was earmarked for foreclosure relief, but the resultant aid programs for homeowners turned out to be riddled with problems, for the perfectly logical reason that none of the bailout’s architects gave a shit about them. They were drawn up practically overnight and rushed out the door for purely political reasons – to trick Congress into handing over tons of instant cash for Wall Street, with no strings attached. “Without those assurances, the level of opposition would have remained the same,” says Rep. Raúl Grijalva, a leading progressive who voted against TARP. The promise of housing aid, in particular, turned out to be a “paper tiger.”

HAMP, the signature program to aid poor homeowners, was announced by President Obama on February 18th, 2009. The move inspired CNBC commentator Rick Santelli to go berserk the next day – the infamous viral rant that essentially birthed the Tea Party. Reacting to the news that Obama was planning to use bailout funds to help poor and (presumably) minority homeowners facing foreclosure, Santelli fumed that the president wanted to “subsidize the losers’ mortgages” when he should “reward people that could carry the water, instead of drink the water.” The tirade against “water drinkers” led to the sort of spontaneous nationwide protests one might have expected months before, when we essentially gave a taxpayer-funded blank check to Gamblers Anonymous addicts, the millionaire and billionaire class.

In fact, the amount of money that eventually got spent on homeowner aid now stands as a kind of grotesque joke compared to the Himalayan mountain range of cash that got moved onto the balance sheets of the big banks more or less instantly in the first months of the bailouts. At the start, $50 billion of TARP funds were earmarked for HAMP. In 2010, the size of the program was cut to $30 billion. As of November of last year, a mere $4 billion total has been spent for loan modifications and other homeowner aid.

In short, the bailout program designed to help those lazy, job-averse, “water-drinking” minority homeowners – the one that gave birth to the Tea Party – turns out to have comprised about one percent of total TARP spending. “It’s amazing,” says Paul Kiel, who monitors bailout spending for ProPublica. “It’s probably one of the biggest failures of the Obama administration.”

The failure of HAMP underscores another damning truth – that the Bush-Obama bailout was as purely bipartisan a program as we’ve had. Imagine Obama retaining Don Rumsfeld as defense secretary and still digging for WMDs in the Iraqi desert four years after his election: That’s what it was like when he left Tim Geithner, one of the chief architects of Bush’s bailout, in command of the no-stringsattached rescue four years after Bush left office.

Yet Obama’s HAMP program, as lame as it turned out to be, still stands out as one of the few pre-bailout promises that was even partially fulfilled. Virtually every other promise Summers made in his letters turned out to be total bullshit. And that includes maybe the most important promise of all – the pledge to use the bailout money to put people back to work.

They Lied About Lending

Once TARP passed, the government quickly began loaning out billions to some 500 banks that it deemed “healthy” and “viable.” A few were cash loans, repayable at five percent within the first five years; other deals came due when a bank stock hit a predetermined price. As long as banks held TARP money, they were barred from paying out big cash bonuses to top executives.

But even before Summers promised Congress that banks would be required to increase lending as a condition for receiving bailout funds, officials had already decided not to even ask the banks to use the money to increase lending. In fact, they’d decided not to even ask banks to monitor what they did with the bailout money. Barofsky, the TARP inspector, asked Treasury to include a requirement forcing recipients to explain what they did with the taxpayer money. He was stunned when TARP administrator Kashkari rejected his proposal, telling him lenders would walk away from the program if they had to deal with too many conditions. “The banks won’t participate,” Kashkari said.

Barofsky, a former high-level drug prosecutor who was one of the only bailout officials who didn’t come from Wall Street, didn’t buy that cash-desperate banks would somehow turn down billions in aid. “It was like they were trembling with fear that the banks wouldn’t take the money,” he says. “I never found that terribly convincing.”

In the end, there was no lending requirement attached to any aspect of the bailout, and there never would be. Banks used their hundreds of billions for almost every purpose under the sun – everything, that is, but lending to the homeowners and small businesses and cities they had destroyed. And one of the most disgusting uses they found for all their billions in free government money was to help them earn even more free government money.

To guarantee their soundness, all major banks are required to keep a certain amount of reserve cash at the Fed. In years past, that money didn’t earn interest, for the logical reason that banks shouldn’t get paid to stay solvent. But in 2006 – arguing that banks were losing profits on cash parked at the Fed – regulators agreed to make small interest payments on the money. The move wasn’t set to go into effect until 2011, but when the crash hit, a section was written into TARP that launched the interest payments in October 2008.

In theory, there should never be much money in such reserve accounts, because any halfway-competent bank could make far more money lending the cash out than parking it at the Fed, where it earns a measly quarter of a percent. In August 2008, before the bailout began, there were just $2 billion in excess reserves at the Fed. But by that October, the number had ballooned to $267 billion – and by January 2009, it had grown to $843 billion. That means there was suddenly more money sitting uselessly in Fed accounts than Congress had approved for either the TARP bailout or the much-loathed Obama stimulus. Instead of lending their new cash to struggling homeowners and small businesses, as Summers had promised, the banks were literally sitting on it.

Today, excess reserves at the Fed total an astonishing $1.4 trillion.”The money is just doing nothing,” says Nomi Prins, a former Goldman executive who has spent years monitoring the distribution of bailout money.

Nothing, that is, except earning a few crumbs of risk-free interest for the banks. Prins estimates that the annual haul in interest on Fed reserves is about $3.6 billion – a relatively tiny subsidy in the scheme of things, but one that, ironically, just about matches the total amount of bailout money spent on aid to homeowners. Put another way, banks are getting paid about as much every year for not lending money as 1 million Americans received for mortgage modifications and other housing aid in the whole of the past four years.

Moreover, instead of using the bailout money as promised – to jump-start the economy – Wall Street used the funds to make the economy more dangerous. From the start, taxpayer money was used to subsidize a string of finance mergers, from the Chase-Bear Stearns deal to the Wells FargoWachovia merger to Bank of America’s acquisition of Merrill Lynch. Aided by bailout funds, being Too Big to Fail was suddenly Too Good to Pass Up.

Other banks found more creative uses for bailout money. In October 2010, Obama signed a new bailout bill creating a program called the Small Business Lending Fund, in which firms with fewer than $10 billion in assets could apply to share in a pool of $4 billion in public money. As it turned out, however, about a third of the 332 companies that took part in the program used at least some of the money to repay their original TARP loans. Small banks that still owed TARP money essentially took out cheaper loans from the government to repay their more expensive TARP loans – a move that conveniently exempted them from the limits on executive bonuses mandated by the bailout. All told, studies show, $2.2 billion of the $4 billion ended up being spent not on small-business loans, but on TARP repayment. “It’s a bit of a shell game,” admitted John Schmidt, chief operating officer of Iowa-based Heartland Financial, which took $81.7 million from the SBLF and used every penny of it to repay TARP.

Using small-business funds to pay down their own debts, parking huge amounts of cash at the Fed in the midst of a stalled economy – it’s all just evidence of what most Americans know instinctively: that the bailouts didn’t result in much new business lending. If anything, the bailouts actually hindered lending, as banks became more like house pets that grow fat and lazy on two guaranteed meals a day than wild animals that have to go out into the jungle and hunt for opportunities in order to eat. The Fed’s own analysis bears this out: In the first three months of the bailout, as taxpayer billions poured in, TARP recipients slowed down lending at a rate more than double that of banks that didn’t receive TARP funds. The biggest drop in lending – 3.1 percent – came from the biggest bailout recipient, Citigroup. A year later, the inspector general for the bailout found that lending among the nine biggest TARP recipients “did not, in fact, increase.” The bailout didn’t flood the banking system with billions in loans for small businesses, as promised. It just flooded the banking system with billions for the banks.

They Lied About the Health of the Banks

The main reason banks didn’t lend out bailout funds is actually pretty simple: Many of them needed the money just to survive. Which leads to another of the bailout’s broken promises – that taxpayer money would only be handed out to “viable” banks.

Soon after TARP passed, Paulson and other officials announced the guidelines for their unilaterally changed bailout plan. Congress had approved $700 billion to buy up toxic mortgages, but $250 billion of the money was now shifted to direct capital injections for banks. (Although Paulson claimed at the time that handing money directly to the banks was a faster way to restore market confidence than lending it to homeowners, he later confessed that he had been contemplating the direct-cash-injection plan even before the vote.) This new let’s-just-fork-over-cash portion of the bailout was called the Capital Purchase Program. Under the CPP, nine of America’s largest banks – including Citi, Wells Fargo, Goldman, Morgan Stanley, Bank of America, State Street and Bank of New York Mellon – received $125 billion, or half of the funds being doled out. Since those nine firms accounted for 75 percent of all assets held in America’s banks – $11 trillion – it made sense they would get the lion’s share of the money. But in announcing the CPP, Paulson and Co. promised that they would only be stuffing cash into “healthy and viable” banks. This, at the core, was the entire justification for the bailout: That the huge infusion of taxpayer cash would not be used to rescue individual banks, but to kick-start the economy as a whole by helping healthy banks start lending again.

This announcement marked the beginning of the legend that certain Wall Street banks only took the bailout money because they were forced to – they didn’t need all those billions, you understand, they just did it for the good of the country. “We did not, at that point, need TARP,” Chase chief Jamie Dimon later claimed, insisting that he only took the money “because we were asked to by the secretary of Treasury.” Goldman chief Lloyd Blankfein similarly claimed that his bank never needed the money, and that he wouldn’t have taken it if he’d known it was “this pregnant with potential for backlash.” A joint statement by Paulson, Bernanke and FDIC chief Sheila Bair praised the nine leading banks as “healthy institutions” that were taking the cash only to “enhance the overall performance of the U.S. economy.”

But right after the bailouts began, soon-to-be Treasury Secretary Tim Geithner admitted to Barofsky, the inspector general, that he and his cohorts had picked the first nine bailout recipients because of their size, without bothering to assess their health and viability. Paulson, meanwhile, later admitted that he had serious concerns about at least one of the nine firms he had publicly pronounced healthy. And in November 2009, Bernanke gave a closed-door interview to the Financial Crisis Inquiry Commission, the body charged with investigating the causes of the economic meltdown, in which he admitted that 12 of the 13 most prominent financial companies in America were on the brink of failure during the time of the initial bailouts.

On the inside, at least, almost everyone connected with the bailout knew that the top banks were in deep trouble. “It became obvious pretty much as soon as I took the job that these companies weren’t really healthy and viable,” says Barofsky, who stepped down as TARP inspector in 2011.

This early episode would prove to be a crucial moment in the history of the bailout. It set the precedent of the government allowing unhealthy banks to not only call themselves healthy, but to get the government to endorse their claims. Projecting an image of soundness was, to the government, more important than disclosing the truth. Officials like Geithner and Paulson seemed to genuinely believe that the market’s fears about corruption in the banking system was a bigger problem than the corruption itself. Time and again, they justified TARP as a move needed to “bolster confidence” in the system – and a key to that effort was keeping the banks’ insolvency a secret. In doing so, they created a bizarre new two-tiered financial market, divided between those who knew the truth about how bad things were and those who did not.

A month or so after the bailout team called the top nine banks “healthy,” it became clear that the biggest recipient, Citigroup, had actually flat-lined on the ER table. Only weeks after Paulson and Co. gave the firm $25 billion in TARP funds, Citi – which was in the midst of posting a quarterly loss of more than $17 billion – came back begging for more. In November 2008, Citi received another $20 billion in cash and more than $300 billion in guarantees.

What’s most amazing about this isn’t that Citi got so much money, but that government-endorsed, fraudulent health ratings magically became part of its bailout. The chief financial regulators – the Fed, the FDIC and the Office of the Comptroller of the Currency – use a ratings system called CAMELS to measure the fitness of institutions. CAMELS stands for Capital, Assets, Management, Earnings, Liquidity and Sensitivity to risk, and it rates firms from one to five, with one being the best and five the crappiest. In the heat of the crisis, just as Citi was receiving the second of what would turn out to be three massive federal bailouts, the bank inexplicably enjoyed a three rating – the financial equivalent of a passing grade. In her book, Bull by the Horns, then-FDIC chief Sheila Bair recounts expressing astonishment to OCC head John Dugan as to why “Citi rated as a CAMELS 3 when it was on the brink of failure.” Dugan essentially answered that “since the government planned on bailing Citi out, the OCC did not plan to change its supervisory rating.” Similarly, the FDIC ended up granting a “systemic risk exception” to Citi, allowing it access to FDIC-bailout help even though the agency knew the bank was on the verge of collapse.

The sweeping impact of these crucial decisions has never been fully appreciated. In the years preceding the bailouts, banks like Citi had been perpetuating a kind of fraud upon the public by pretending to be far healthier than they really were. In some cases, the fraud was outright, as in the case of Lehman Brothers, which was using an arcane accounting trick to book tens of billions of loans as revenues each quarter, making it look like it had more cash than it really did. In other cases, the fraud was more indirect, as in the case of Citi, which in 2007 paid out the third-highest dividend in America – $10.7 billion – despite the fact that it had lost $9.8 billion in the fourth quarter of that year alone. The whole financial sector, in fact, had taken on Ponzi-like characteristics, as many banks were hugely dependent on a continual influx of new money from things like sales of subprime mortgages to cover up massive future liabilities from toxic investments that, sooner or later, were going to come to the surface.

Now, instead of using the bailouts as a clear-the-air moment, the government decided to double down on such fraud, awarding healthy ratings to these failing banks and even twisting its numerical audits and assessments to fit the cooked-up narrative. A major component of the original TARP bailout was a promise to ensure “full and accurate accounting” by conducting regular “stress tests” of the bailout recipients. When Geithner announced his stress-test plan in February 2009, a reporter instantly blasted him with an obvious and damning question: Doesn’t the fact that you have to conduct these tests prove that bank regulators, who should already know plenty about banks’ solvency, actually have no idea who is solvent and who isn’t?

The government did wind up conducting regular stress tests of all the major bailout recipients, but the methodology proved to be such an obvious joke that it was even lampooned on Saturday Night Live. (In the skit, Geithner abandons a planned numerical score system because it would unfairly penalize bankers who were “not good at banking.”) In 2009, just after the first round of tests was released, it came out that the Fed had allowed banks to literally rejigger the numbers to make their bottom lines look better. When the Fed found Bank of America had a $50 billion capital hole, for instance, the bank persuaded examiners to cut that number by more than $15 billion because of what it said were “errors made by examiners in the analysis.” Citigroup got its number slashed from $35 billion to $5.5 billion when the bank pleaded with the Fed to give it credit for “pending transactions.”

Such meaningless parodies of oversight continue to this day. Earlier this year, Regions Financial Corp. – a company that had failed to pay back $3.5 billion in TARP loans – passed its stress test. A subsequent analysis by Bloomberg View found that Regions was effectively $525 million in the red. Nonetheless, the bank’s CEO proclaimed that the stress test “demonstrates the strength of our company.” Shortly after the test was concluded, the bank issued $900 million in stock and said it planned on using the cash to pay back some of the money it had borrowed under TARP.

This episode underscores a key feature of the bailout: the government’s decision to use lies as a form of monetary aid. State hands over taxpayer money to functionally insolvent bank; state gives regulatory thumbs up to said bank; bank uses that thumbs up to sell stock; bank pays cash back to state. What’s critical here is not that investors actually buy the Fed’s bullshit accounting – all they have to do is believe the government will backstop Regions either way, healthy or not. “Clearly, the Fed wanted it to attract new investors,” observed Bloomberg, “and those who put fresh capital into Regions this week believe the government won’t let it die.”

Through behavior like this, the government has turned the entire financial system into a kind of vast confidence game – a Ponzi-like scam in which the value of just about everything in the system is inflated because of the widespread belief that the government will step in to prevent losses. Clearly, a government that’s already in debt over its eyes for the next million years does not have enough capital on hand to rescue every Citigroup or Regions Bank in the land should they all go bust tomorrow. But the market is behaving as if Daddy will step in to once again pay the rent the next time any or all of these kids sets the couch on fire and skips out on his security deposit. Just like an actual Ponzi scheme, it works only as long as they don’t have to make good on all the promises they’ve made. They’re building an economy based not on real accounting and real numbers, but on belief. And while the signs of growth and recovery in this new faith-based economy may be fake, one aspect of the bailout has been consistently concrete: the broken promises over executive pay.

They Lied About Bonuses

hat executive bonuses on Wall Street were a political hot potato for the bailout’s architects was obvious from the start. That’s why Summers, in saving the bailout from the ire of Congress, vowed to “limit executive compensation” and devote public money to prevent another financial crisis. And it’s true, TARP did bar recipients from a whole range of exorbitant pay practices, which is one reason the biggest banks, like Goldman Sachs, worked so quickly to repay their TARP loans.

But there were all sorts of ways around the restrictions. Banks could apply to the Fed and other regulators for waivers, which were often approved (one senior FDIC official tells me he recommended denying “golden parachute” payments to Citigroup officials, only to see them approved by superiors). They could get bailouts through programs other than TARP that did not place limits on bonuses. Or they could simply pay bonuses not prohibited under TARP. In one of the worst episodes, the notorious lenders Fannie Mae and Freddie Mac paid out more than $200 million in bonuses between 2008 and 2010, even though the firms (a) lost more than $100 billion in 2008 alone, and (b) required nearly $400 billion in federal assistance during the bailout period.

Even worse was the incredible episode in which bailout recipient AIG paid more than $1 million each to 73 employees of AIG Financial Products, the tiny unit widely blamed for having destroyed the insurance giant (and perhaps even triggered the whole crisis) with its reckless issuance of nearly half a trillion dollars in toxic credit-default swaps. The “retention bonuses,” paid after the bailout, went to 11 employees who no longer worked for AIG.

But all of these “exceptions” to the bonus restrictions are far less infuriating, it turns out, than the rule itself. TARP did indeed bar big cash-bonus payouts by firms that still owed money to the government. But those firms were allowed to issue extra compensation to executives in the form of long-term restricted stock. An independent research firm asked to analyze the stock options for The New York Times found that the top five executives at each of the 18 biggest bailout recipients received a total of $142 million in stocks and options. That’s plenty of money all by itself – but thanks in large part to the government’s overt display of support for those firms, the value of those options has soared to $457 million, an average of $4 million per executive.

In other words, we didn’t just allow banks theoretically barred from paying bonuses to pay bonuses. We actually allowed them to pay bigger bonuses than they otherwise could have. Instead of forcing the firms to reward top executives in cash, we allowed them to pay in depressed stock, the value of which we then inflated due to the government’s implicit endorsement of those firms.

All of which leads us to the last and most important deception of the bailouts:

They Lied About the Bailout Being Temporary

The bailout ended up being much bigger than anyone expected, expanded far beyond TARP to include more obscure (and in some cases far larger) programs with names like TALF, TAF, PPIP and TLGP. What’s more, some parts of the bailout were designed to extend far into the future. Companies like AIG, GM and Citigroup, for instance, were given tens of billions of deferred tax assets – allowing them to carry losses from 2008 forward to offset future profits and keep future tax bills down. Official estimates of the bailout’s costs do not include such ongoing giveaways. “This is stuff that’s never going to appear on any report,” says Barofsky.

Citigroup, all by itself, boasts more than $50 billion in deferred tax credits – which is how the firm managed to pay less in taxes in 2011 (it actually received a $144 million credit) than it paid in compensation that year to its since-ousted dingbat CEO, Vikram Pandit (who pocketed $14.9 million). The bailout, in short, enabled the very banks and financial institutions that cratered the global economy to write off the losses from their toxic deals for years to come – further depriving the government of much-needed tax revenues it could have used to help homeowners and small businesses who were screwed over by the banks in the first place.

Even worse, the $700 billion in TARP loans ended up being dwarfed by more than $7.7 trillion in secret emergency lending that the Fed awarded to Wall Street – loans that were only disclosed to the public after Congress forced an extraordinary one-time audit of the Federal Reserve. The extent of this “secret bailout” didn’t come out until November 2011, when Bloomberg Markets, which went to court to win the right to publish the data, detailed how the country’s biggest firms secretly received trillions in near-free money throughout the crisis.

Goldman Sachs, which had made such a big show of being reluctant about accepting $10 billion in TARP money, was quick to cash in on the secret loans being offered by the Fed. By the end of 2008, Goldman had snarfed up $34 billion in federal loans – and it was paying an interest rate of as low as just 0.01 percent for the huge cash infusion. Yet that funding was never disclosed to shareholders or taxpayers, a fact Goldman confirms. “We did not disclose the amount of our participation in the two programs you identify,” says Goldman spokesman Michael Duvally.

Goldman CEO Blankfein later dismissed the importance of the loans, telling the Financial Crisis Inquiry Commission that the bank wasn’t “relying on those mechanisms.” But in his book, Bailout, Barofsky says that Paulson told him that he believed Morgan Stanley was “just days” from collapse before government intervention, while Bernanke later admitted that Goldman would have been the next to fall.

Meanwhile, at the same moment that leading banks were taking trillions in secret loans from the Fed, top officials at those firms were buying up stock in their companies, privy to insider info that was not available to the public at large. Stephen Friedman, a Goldman director who was also chairman of the New York Fed, bought more than $4 million of Goldman stock over a five-week period in December 2008 and January 2009 – years before the extent of the firm’s lifeline from the Fed was made public. Citigroup CEO Vikram Pandit bought nearly $7 million in Citi stock in November 2008, just as his firm was secretly taking out $99.5 billion in Fed loans. Jamie Dimon bought more than $11 million in Chase stock in early 2009, at a time when his firm was receiving as much as $60 billion in secret Fed loans. When asked by Rolling Stone, Chase could not point to any disclosure of the bank’s borrowing from the Fed until more than a year later, when Dimon wrote about it in a letter to shareholders in March 2010.

The stock purchases by America’s top bankers raise serious questions of insider trading. Two former high-ranking financial regulators tell Rolling Stone that the secret loans were likely subject to a 1989 guideline, issued by the Securities and Exchange Commission in the heat of the savings and loan crisis, which said that financial institutions should disclose the “nature, amounts and effects” of any government aid. At the end of 2011, in fact, the SEC sent letters to Citigroup, Chase, Goldman Sachs, Bank of America and Wells Fargo asking them why they hadn’t fully disclosed their secret borrowing. All five megabanks essentially replied, to varying degrees of absurdity, that their massive borrowing from the Fed was not “material,” or that the piecemeal disclosure they had engaged in was adequate. Never mind that the law says investors have to be informed right away if CEOs like Dimon and Pandit decide to give themselves a $10,000 raise. According to the banks, it’s none of your business if those same CEOs are making use of a secret $50 billion charge card from the Fed.

The implications here go far beyond the question of whether Dimon and Co. committed insider trading by buying and selling stock while they had access to material nonpublic information about the bailouts. The broader and more pressing concern is the clear implication that by failing to act, federal regulators have tacitly approved the nondisclosure. Instead of trusting the markets to do the right thing when provided with accurate information, the government has instead channeled Jack Nicholson – and decided that the public just can’t handle the truth.

All of this – the willingness to call dying banks healthy, the sham stress tests, the failure to enforce bonus rules, the seeming indifference to public disclosure, not to mention the shocking lack of criminal investigations into fraud committed by bailout recipients before the crash – comprised the largest and most valuable bailout of all. Brick by brick, statement by reassuring statement, bailout officials have spent years building the government’s great Implicit Guarantee to the biggest companies on Wall Street: We will be there for you, always, no matter how much you screw up. We will lie for you and let you get away with just about anything. We will make this ongoing bailout a pervasive and permanent part of the financial system. And most important of all, we will publicly commit to this policy, being so obvious about it that the markets will be able to put an exact price tag on the value of our preferential treatment.

The first independent study that attempted to put a numerical value on the Implicit Guarantee popped up about a year after the crash, in September 2009, when Dean Baker and Travis McArthur of the Center for Economic and Policy Research published a paper called “The Value of the ‘Too Big to Fail’ Big Bank Subsidy.” Baker and McArthur found that prior to the last quarter of 2007, just before the start of the crisis, financial firms with $100 billion or more in assets were paying on average about 0.29 percent less to borrow money than smaller firms.

By the second quarter of 2009, however, once the bailouts were in full swing, that spread had widened to 0.78 percent. The conclusion was simple: Lenders were about a half a point more willing to lend to a bank with implied government backing – even a proven-stupid bank – than they were to lend to companies who “must borrow based on their own credit worthiness.” The economists estimated that the lending gap amounted to an annual subsidy of $34 billion a year to the nation’s 18 biggest banks.

Today the borrowing advantage of a big bank remains almost exactly what it was three years ago – about 50 basis points, or half a percent. “These megabanks still receive subsidies in the sense that they can borrow on the capital markets at a discount rate of 50 or 70 points because of the implicit view that these banks are Too Big to Fail,” says Sen. Brown.

Why does the market believe that? Because the officials who administered the bailouts made that point explicitly, over and over again. When Geithner announced the implementation of the stress tests in 2009, for instance, he declared that banks who didn’t have enough money to pass the test could get it from the government. “We’re going to help this process by providing a new program of capital support for those institutions that need it,” Geithner said. The message, says Barofsky, was clear: “If the banks cannot raise capital, we will do it for them.” It was an Implicit Guarantee that the banks would not be allowed to fail – a point that Geithner and other officials repeatedly stressed over the years. “The markets took all those little comments by Geithner as a clue that the government is looking out for them,” says Baker. That psychological signaling, he concludes, is responsible for the crucial half-point borrowing spread.

The inherent advantage of bigger banks – the permanent, ongoing bailout they are still receiving from the government – has led to a host of gruesome consequences. All the big banks have paid back their TARP loans, while more than 300 smaller firms are still struggling to repay their bailout debts. Even worse, the big banks, instead of breaking down into manageable parts and becoming more efficient, have grown even bigger and more unmanageable, making the economy far more concentrated and dangerous than it was before. America’s six largest banks – Bank of America, JP Morgan Chase, Citigroup, Wells Fargo, Goldman Sachs and Morgan Stanley – now have a combined 14,420 subsidiaries, making them so big as to be effectively beyond regulation. A recent study by the Kansas City Fed found that it would take 70,000 examiners to inspect such trillion-dollar banks with the same level of attention normally given to a community bank. “The complexity is so overwhelming that no regulator can follow it well enough to regulate the way we need to,” says Sen. Brown, who is drafting a bill to break up the megabanks.

Worst of all, the Implicit Guarantee has led to a dangerous shift in banking behavior. With an apparently endless stream of free or almost-free money available to banks – coupled with a well-founded feeling among bankers that the government will back them up if anything goes wrong – banks have made a dramatic move into riskier and more speculative investments, including everything from high-risk corporate bonds to mortgagebacked securities to payday loans, the sleaziest and most disreputable end of the financial system. In 2011, banks increased their investments in junk-rated companies by 74 percent, and began systematically easing their lending standards in search of more high-yield customers to lend to.

This is a virtual repeat of the financial crisis, in which a wave of greed caused bankers to recklessly chase yield everywhere, to the point where lowering lending standards became the norm. Now the government, with its Implicit Guarantee, is causing exactly the same behavior – meaning the bailouts have brought us right back to where we started. “Government intervention,” says Klaus Schaeck, an expert on bailouts who has served as a World Bank consultant, “has definitely resulted in increased risk.”

And while the economy still mostly sucks overall, there’s never been a better time to be a Too Big to Fail bank. Wells Fargo reported a third-quarter profit of nearly $5 billion last year, while JP Morgan Chase pocketed $5.3 billion – roughly double what both banks earned in the third quarter of 2006, at the height of the mortgage bubble. As the driver of their success, both banks cite strong performance in – you guessed it – the mortgage market.

So what exactly did the bailout accomplish? It built a banking system that discriminates against community banks, makes Too Big to Fail banks even Too Bigger to Failier, increases risk, discourages sound business lending and punishes savings by making it even easier and more profitable to chase high-yield investments than to compete for small depositors. The bailout has also made lying on behalf of our biggest and most corrupt banks the official policy of the United States government. And if any one of those banks fails, it will cause another financial crisis, meaning we’re essentially wedded to that policy for the rest of eternity – or at least until the markets call our bluff, which could happen any minute now.

Other than that, the bailout was a smashing success.

© 2012 Rolling Stone

As Rolling Stone’s chief political reporter, Matt Taibbi’s predecessors include the likes of journalistic giants Hunter S. Thompson and P.J. O’Rourke. Taibbi’s 2004 campaign journal Spanking the Donkey cemented his status as an incisive, irreverent, zero-bullshit reporter. His books include Griftopia: A Story of Bankers, Politicians, and the Most Audacious Power Grab in American History, The Great Derangement: A Terrifying True Story of War, Politics, and Religion, Smells Like Dead Elephants: Dispatches from a Rotting Empire.

Foreclosure Fiasco Continues: The Bush-Obama Strategy of Throwing Billions at Banks Doesn’t Work June 27, 2009

Posted by rogerhollander in Uncategorized.Tags: bailout, Ben Bernanke, Bush, citigroup, commodity futures, economy, Federal Reserve, food banks, foreclosure, gary gensler, gene sperling, glass-steagall, Goldman Sachs, Larry Summers, mortgage, mortgage crisis, ned, Obama, obama administration, poverty, Robert Scheer, roger hollander, Wall Street

add a comment

By Robert Scheer, Truthdig. Posted June 27, 2009.

Americans are now $14 trillion poorer. Many who thought they were middle class have now joined the ranks of the poor.

It’s not working. The Bush-Obama strategy of throwing trillions at the banks to solve the mortgage crisis is a huge bust. The financial moguls, while tickled pink to have $1.25 trillion in toxic assets covered by the feds, along with hundreds of billions in direct handouts, are not using that money to turn around the free fall in housing foreclosures.

As The Wall Street Journal reported Tuesday, “The Mortgage Bankers Association cut its forecast of home-mortgage lending this year by 27% amid deflating hopes for a boom in refinancing.” The same association said that the total refinancing under the administration’s much ballyhooed Home Affordable Refinance Program is “very low.”

Aside from a tight mortgage market, the problem in preventing foreclosures has to do with homeowners losing their jobs. Here again the administration, continuing the Bush strategy, is working the wrong end of the problem. Although President Obama was wise enough to at least launch a job stimulus program, a far greater amount of federal funding benefits Wall Street as opposed to Main Street.

State and local governments have been forced into draconian budget cuts, firing workers who are among the most reliable in making their mortgage payments–when they have jobs. Yet the Obama administration won’t spend even a small fraction of what it has wasted on the banks to cover state shortfalls.

California couldn’t get the White House to guarantee $5.5 billion in short-term notes to avert severe cuts in state and local payrolls, from prison guards to schoolteachers. Compare that with the $50 billion already given to Citigroup, plus an astounding $300 billion to guarantee that institution’s toxic assets. Citigroup benefits from being a bank “too big to fail,” although through its irresponsible actions to get that large it did as much as any company to cause this mess.

How big a mess? According to the Federal Reserve’s most recent report, seven straight quarters of declining household wealth have left Americans $14 trillion poorer. Many who thought they were middle class have now joined the ranks of the poor. Food banks are strapped and welfare rolls are dramatically on the rise, as the WSJ reports, with a 27 percent year-to-year increase in Oregon, 23 percent in South Carolina and 10 percent in California. And you have to be very poor to get on welfare, thanks to President Clinton’s so-called welfare reform, which he signed into law before he ramped up the radical deregulation of the financial services industry, enabling our economic downturn.

Citigroup, the prime mover for ending the sensible restraints of the Glass-Steagall Act of 1933, is now a pathetic ward of the state. But back in the day President Clinton would tour the country with Citigroup founder Sandy Weill touting the wonderful work that Weill and other moguls were doing to invest in economically depressed communities. It wasn’t really happening then, and now millions of folks in those communities have seen their houses snatched from them as if they were just pieces in a game of Monopoly that Clinton and his fat-cat buddy were playing.

Once Weill got the radical deregulation law he wanted, he issued a statement giving credit: “In particular, we congratulate President Clinton, Treasury Secretary Larry Summers, NEC [National Economic Council] Chairman Gene Sperling, Under Secretary of the Treasury Gary Gensler, Assistant Treasury Secretaries Linda Robertson and Greg Baer.”

Summers is now Obama’s top economic adviser, Sperling has been appointed legal counselor at Treasury, and Gensler, a former partner in Goldman Sachs, is head of the Commodity Futures Trading Commission, which he once attempted to prevent from regulating derivatives when it was run by Brooksley Born. Robertson worked for Summers in pushing through the Commodity Futures Modernization Act, which freed the derivatives market from adult supervision and contained the “Enron Loophole,” permitting that company to go wild. Robertson then became the top Washington lobbyist for Enron and was recently appointed senior adviser to Fed Chair Ben S. Bernanke. Baer went to work as a corporate counsel for Bank of America, which announced his appointment with a press release crediting him with having “coordinated Treasury policy” during the Clinton years in getting Glass-Steagall repealed. As a result of deregulation, B of A too spiraled out of control and ended up as a beneficiary of the Treasury’s welfare program.

Why was I so naive as to have expected this Democratic president to not do the bidding of the banks when the last president from that party joined the Republicans in giving the moguls everything they wanted? Please, Obama, prove me wrong.

Robert Scheer is Editor in Chief of Truthdig and author of a new book, The Pornography of Power: How Defense Hawks Hijacked 9/11 and Weakened America.

Mortgaging the White House May 2, 2009

Posted by rogerhollander in Economic Crisis.Tags: bailout, bank bailout, banking barons, banksters, bill moyers, citigroup, congressional oversight, cop, economic advisor, Economic Crisis, fdr, Federal Reserve, finance industry, foreclosure, franklin delano roosevelt, geithner, great deression, gretchen morgenson, jo becker, laissez-faire, Larry Summers, michael winship, new york federal reserve, president obama, richard durbin, robert rubin, roger hollander, tarp, tarp bailout, taxpayer, treasury, Wall Street, white house

1 comment so far

Published on Saturday, May 2, 2009 by CommonDreams.org

Finally, here we are at the end of this week of a hundred days. As everyone in the western world probably knows by now, this benchmark for assessing presidencies goes back to Franklin Delano Roosevelt, who arrived at the White House in the depths of the Great Depression.

In his first hundred days, FDR came out swinging. He shut down the banks, threw the money lenders from the temple, cranked out so much legislation so fast he would shout to his secretary, Grace Tully, “Grace, take a law!” Will Rogers said Congress didn’t pass bills anymore; it just waved as they went by.

President Obama’s been busy, but contrary to many of the pundits, he’s no FDR. Our new president got his political education in the world of Chicago ward politics, and seems to have adopted a strategy from the machine of that city’s longtime boss, the late Richard J. Daley, father of the current mayor there. “Don’t make no waves,” one of Daley’s henchmen used to advise, “don’t back no losers.”

Your opinion of Obama’s first 100 days depends of course on your own vantage point. But we’d argue that as part of his bending over backwards to support the banks and avoid the losers, he has blundered mightily in his choice of economic advisers.

Last week, at a hearing of the Congressional Oversight Panel (COP) monitoring the Troubled Asset Relief Program (TARP), Treasury Secretary Timothy Geithner tried to correct AFL-CIO General Counsel Damon Silvers. “I’ve practiced law and you’ve been a banker,” Silvers said. Never, Geithner replied, “I’ve only been in public service.”

We beg to differ. Read Jo Becker and Gretchen Morgenson’s front-page profile of Secretary Geithner in Monday’s New York Times, and you’ll see how Robert Rubin protégé Geithner, during the five years he was running the New York Federal Reserve, fell under the spell of the big barons of banking to whom he would one day help shovel overly generous sums of money at taxpayer expense.

During “an era of unbridled and ultimately disastrous risk-taking by the financial industry,” the Times reported, “… He forged unusually close relationships with executives of Wall Street’s giant financial institutions.

“His actions, as a regulator and later a bailout king, often aligned with the industry’s interests and desires, according to interviews with financiers, regulators and analysts and a review of Federal Reserve records.”

Wined and dined at the Four Seasons, and in corporate dining rooms and fine homes by the very men whose greed and judgment helped bring on the Great Collapse, Geithner became so much a favorite of the Club that former Citigroup chairman Sandy Weill talked with him about becoming the bank’s CEO.

According to Becker and Morgenson, “Even as banks complain that the government has attached too many intrusive strings to its financial assistance, a range of critics — lawmakers, economists and even former Federal Reserve colleagues — say that the bailout Mr. Geithner has played such a central role in fashioning is overly generous to the financial industry at taxpayer expense.”

The two reporters write that Geithner “repeatedly missed or overlooked signs” that the financial system was self-destructing. “When he did spot trouble, analysts say, his responses were too measured, or too late.”

In choosing a man to manage the bailout of the banks who’s so cozy with its players, and then installing as his White House economic adviser Larry Summers, who in the Clinton administration took a laissez-faire attitude toward the financial industry which would later enrich him, the president bought into the old fantasy that what’s best for Wall Street is best for America.

With these two as his financial gatekeepers, President Obama’s now in the position of Louis XVI being advised by Marie Antoinette to have another piece of cake until that rumble in the streets has passed on by.

In fact, other Wall Street insiders — many of them big contributors to the Obama presidential campaign, and progressive in their concern for the public interest — privately are expressing serious concerns that Geithner, Summers and their associates are leading the president and America’s taxpayers down a path toward further economic disaster.

This week, as Senate Majority Whip Richard Durbin of Illinois unsuccessfully fought for a congressional amendment he said would have helped 1.7 million Americans save their homes from foreclosure, the senator told a radio station back home that, “The banks — hard to believe in a time when we’re facing a banking crisis that many of the banks created — are still the most powerful lobby on Capitol Hill. And they frankly own the place.”

He could say the same of the White House.

Banksters on the War Path: How Wall Street Is Fighting Back and Winning Their Fight for the Status Quo May 2, 2009

Posted by rogerhollander in Economic Crisis.Tags: arlen specter, bailout, bankers, banking industry, banksters, capitalism, chrysler, chrysler bankruptcy, danny schechter, democracy, derivatives, dick durbin, Economic Crisis, eric holder, finance industry, financial system, foreclosures, hedge funds, kevin phillips, Larry Summers, Lobbyists, naked capitalism, obama administration, robert rubin, Robert Scheer, roger hollander, senate, subprime mortgages, tarp, tarp bailout, taxpayer, tim geithner, trade unionists, unemployed, us regulators, Wall Street, workers, zogby poll

add a comment

Published on Saturday, May 2, 2009 by CommonDreams.org

Dick Durbin knows his way around the Senate. He’s been there a long time, long enough to know how things really work. Over the years, the man from Illinois has come to realize that it’s not the elected officials who are in charge. Last week, he said it was the bankers “who run the place” acknowledging that Senators may be in office, but not necessarily in power.

Usually, the people who pull the strings stay in the background to avoid too much public exposure. They rely on lobbyists to do their bidding. They prefer to work in the shadows. They may back certain politicians, but coming from a world of credit default swaps as they do, they hedge their bets by putting money on all the horses.

They have so much influence because they have been reengineering the American economy for decades through “financialization,” a process by which banks and financial institutions gradually came to dominate economic and political decision-making. Kevin Phillips, a one time Reagan advisor and commentator, says our deepest problem is “the ascendancy of finance in national policymaking (as well as in the gross domestic product), and the complicity of politicians who really don’t want to talk about it.”

Curiously, despite the journalists like Bill Moyers and Arianna Huffington who have been blowing the whistle on the role of the “banksters” in our political life, criticizing the Republicans and Democrats who deregulated the financial system, this issue seems to float above the heads of most of the public, much of the press, and even the activist community more drawn to punishing the torture inflicted on a few by a former Administration than the economic duress being imposed on the majority of Americans by a minority of the super rich.

Demonstrators are still drawn more to the White House than the banks that have proliferated on every corner of the country.

Last week, a Zogby poll found that a majority of the public believes the press made things worse by reporting on the economic collapse. Not only is that blaming the messenger, it also overlooks the fact that much of the media was complicit in the crisis by not covering the forces that caused the collapse when it might have done some good.

Exacerbating the problem is that the Obama Administration has, in Robert Scheer’s words, enlisted “the very experts who helped trigger the crisis to try to fix it.”

“Obama,” he writes “seems depressingly reliant on the same-old, same old cast of self-serving house wreckers who act as if government exists for the sole benefit of corporations and executives.”

The team of Tim Geithner and Larry Summers has been carrying Wall Street’s water as Robert Rubin did before them. No wonder that Obama’s Attorney General Eric Holder told the Street last February, “We’re not going to go on any witch hunts.”

That was before we learned that Wall Street forced US regulators to delay the release of stress test results for the country’s 19 biggest banks until next Thursday, because some of the lenders objected to government demands that they needed to raise more capital. They are trying to rig the results.

That was also before the public learned of the obscenely huge bonuses the firms benefiting from the TARP bailout were shelling out to their executives. That was before we saw how the bankers with help from Democrats, including new convert Arlen Specter, managed to kill a bill to help homeowners stop foreclosures.

“The Senate on Thursday rejected an effort to stave off home foreclosures by a vote of 51 to 45. It was an overwhelming defeat, with the bill’s backers falling 15 votes short — a quarter of the Democratic caucus — of the 60 needed to cut off debate and move to a final vote. Across the United States, the measure is estimated to have been able to prevent 1.69 million foreclosures and preserve $300 billion in home equity.”

Commented the Center for Responsible Lending, “Instead of defending ordinary Americans, the majority of Senators went with the banks. Yes, the same banks who have benefited so richly from the TARP bailout.”

There was one small victory with the House approving a bill to protect consumers from credit card abuses. It’s not clear if the Senate will pass it too. “It’s one step forward and one step backward,” said Travis Plunkett, of the Consumer Federation of America. “Congress is moving in fits and starts to re-regulate the financial services industry and the banking lobby still has tremendous clout.”

“Tremendous clout” is an understatement.

In this past week, we also saw how a few hedge funds undermined the attempt to save Chrysler from bankruptcy by holding out for more money even after the unions and big banks agreed to compromise to save jobs.

The President was furious but apparently powerless: “A group of investment firms and hedge funds decided to hold out for the prospect of an unjustified taxpayer-funded bailout,” Obama said. “They were hoping that everybody else would make sacrifices, and they would have to make none. Some demanded twice the return that other lenders were getting.”

Explains the blog Naked Capitalism, “the banksters are eagerly, shamelessly, and openly harvesting their pound of flesh from financially stressed average taxpayers, and setting off a chain reaction in the auto industry which has the very real risk of creating even larger scale unemployment than the economy already faces. It’s reckless, utterly irresponsible, over-the-top greed.”

Will they be allowed to get away with it? A “captured” Congress is doing their bidding. There is no doubt that class antagonism is stewing, says the editor of the blog. He expressed a fear of a reaction that will go way beyond flag-wavng tea parties.

“… I am concerned this behavior is setting the stage for another sort of extra-legal measure: violence. I have been amazed at the vitriol directed at the banking classes. Suggestions for punishment have included the guillotine (frequent), hanging, pitchforks, even burning at the stake. Tar and feathering appears inadequate, and stoning hasn’t yet surfaced as an idea. And mind you, my readership is educated, older, typically well-off (even if less so than three years ago). The fuse has to be shorter where the suffering is more acute.”

One is reminded of the title of that movie, “There will be blood.” Rather than show contrition or compassion for its own victims, Wall Street is hoping to jack up its salaries and bonuses to pre-2007 levels. The men at the top are oblivious to the pain they helped cause. And so far, they’ve only occasionally been scolded by politicians that have mostly enabled, coddled, bankrolled, funded, rewarded, and genuflected to their power.

Wall Street’s behavior may be predictable, but how can we account for the silence of so many organizations that should be out there organizing the outrage that is building? Knock, Knock, Obama supporters, bloggers, trade unionists, out of work workers and fellow Americans. Will we fight back or roll over?

Pitchforks anyone?

Tsunami Of Populist Rage Coursing Through America February 8, 2009

Posted by rogerhollander in Economic Crisis.Tags: AIG, Alston & Bird, bank rescue, bob dole, ceo bonus, citygroup, crony capitalism, deregulation, derivative markets, Economic Crisis, economic meltdown, frank rich, Goldman Sachs, great depression, Hank Paulson, health care reform, income inequality, job loss, Joe the Plumber, Larry Summers, McCain, ordinary americans, Palin, paul volcker, Pepsi and Viagra, Phil Gramm, president obama, public anger, Rahm Emanuel, retirement savings, revolving door, Robert Reich, roger hollander, salary caps, slumdog milionaire, tarp, tax delinquency, tax evasion, timothy geithner, tom daschle, treasury secretary, unemployment

add a comment

Slumdogs Unite!

Frank Rich

SOMEDAY historians may look back at Tom Daschle’s flameout as a minor one-car (and chauffeur) accident. But that will depend on whether or not it’s followed by a multi-vehicle pileup that still could come. Even as President Obama refreshingly took responsibility for having “screwed up,” it’s not clear that he fully understands the huge forces that hit his young administration last week.

Like nearly everyone else in Washington, Obama was blindsided by the savagery and speed of Daschle’s demise. Conventional wisdom had him surviving the storm. Such is the city’s culture that not a single Republican or Democratic senator called for his withdrawal until the morning of his exit. Membership in the exclusive Senate club, after all, has its privileges. Among Daschle’s more vocal defenders was Bob Dole, who had recruited him to Alston & Bird, the law and lobbying firm where Dole has served as “special counsel” when not otherwise cashing in on his own Senate years by serving as a pitchman for Pepsi and Viagra.

In New York, editorial pages on both ends of the political spectrum, The Wall Street Journal and The Times, called for Daschle to step down. But not The Washington Post. In a frank expression of the capital’s isolation from the country, it thought Daschle could still soldier on even though “ordinary Americans who pay their taxes may well wonder why Mr. Obama can’t find cabinet secretaries who do the same.”

As Jon Stewart might say, oh those pesky ordinary Americans!

In reality, Daschle’s tax shortfall, an apparently honest mistake, was only a red flag for the larger syndrome that much of Washington still doesn’t get. It was the source, not the amount, of his unreported income that did him in. The car and driver advertised his post-Senate immersion in the greedy bipartisan culture of entitlement and crony capitalism that both helped create our economic meltdown (on Wall Street) and failed to police it (in Washington). Daschle might well have been the best choice to lead health-care reform. But his honorable public record was instantly vaporized by tales of his cozy, lucrative relationships with the very companies he’d have to adjudicate as health czar.

Few articulate this ethical morass better than Obama, who has repeatedly vowed to “close the revolving door” between business and government and end our “two sets of standards, one for powerful people and one for ordinary folks.” But his tough new restrictions on lobbyists (already compromised by inexplicable exceptions) and porous plan for salary caps on bailed-out bankers are only a down payment on this promise, even if they are strictly enforced.

The new president who vowed to change Washington’s culture will have to fight much harder to keep from being co-opted by it instead. There are simply too many major players in the Obama team who are either alumni of the financial bubble’s insiders’ club or of the somnambulant governmental establishment that presided over the catastrophe.

This includes Timothy Geithner, the Treasury secretary. Washington hands repeatedly observe how “lucky” Geithner was to be the first cabinet nominee with an I.R.S. problem, not the second, and therefore get confirmed by Congress while the getting was good. Whether or not this is “lucky” for him, it is hardly lucky for Obama. Geithner should have left ahead of Daschle.

Now more than ever, the president must inspire confidence and stave off panic. As Friday’s new unemployment figures showed, the economy kept plummeting while Congress postured. Though Obama is a genius at building public support, he is not Jesus and he can’t do it all alone. On Monday, it’s Geithner who will unveil the thorniest piece of the economic recovery plan to date — phase two of a bank rescue. The public face of this inevitably controversial package is now best known as the guy who escaped the tax reckoning that brought Daschle down.

Even before the revelation of his tax delinquency, the new Treasury secretary was a dubious choice to make this pitch. Geithner was present at the creation of the first, ineffectual and opaque bank bailout — TARP, today the most radioactive acronym in American politics. Now the double standard that allowed him to wriggle out of his tax mess is a metaphor for the double standard of the policy he must sell: Most “ordinary Americans” still don’t understand why banks got billions while nothing was done (and still isn’t being done) to bail out those who lost their homes, jobs and retirement savings.

As with Daschle, the political problems caused by Geithner’s tax infraction are secondary to the larger questions raised by his past interaction with the corporations now under his purview. To his credit, Geithner, like Obama, has devoted his career to public service, not buckraking. But he still has not satisfactorily explained why, as president of the New York Fed, he failed in his oversight of the teetering Wall Street institutions. Nor has he told us why, in his first major move in his new job, he secured a waiver from Obama to hire a Goldman Sachs lobbyist as his chief of staff. Nor, in his confirmation hearings, did he prove any more credible than the Bush Treasury secretary, the Goldman Sachs alumnus Hank Paulson, in explaining why Lehman Brothers was allowed to fail while A.I.G. and Citigroup were spared.

Citigroup had one highly visible asset that Lehman did not: Robert Rubin, the former Clinton Treasury secretary who sat passively (though lucratively) in its executive suite as Citi gorged on reckless risk. Geithner, as a Rubin protégé from the Clinton years, might have recused himself from rescuing Citi, which so far has devoured $45 billion in bailout money.

Key players in the Obama economic team beyond Geithner are also tied to Rubin or Citigroup or both, from Larry Summers, the administration’s top economic adviser, to Gary Gensler, the newly named nominee to run the Commodity Futures Trading Commission and a Treasury undersecretary in the Clinton administration. Back then, Summers and Gensler joined hands with Phil Gramm to ward off regulation of the derivative markets that have since brought the banking system to ruin. We must take it on faith that they have subsequently had judgment transplants.

Obama’s brilliant appointees, we keep being told, are irreplaceable. But as de Gaulle said, “The cemeteries of the world are full of indispensable men.” You have to wonder if this team is really a meritocracy or merely a stacked deck. Not only did Rubin himself serve on the Obama economic transition team, but two of the transition’s headhunters were Michael Froman, Rubin’s chief of staff at Treasury and later a Citigroup executive, and James S. Rubin, an investor who is Robert Rubin’s son.

A welcome outlier to this club is Paul Volcker, the former Federal Reserve chairman chosen to direct Obama’s Economic Recovery Advisory Board. But Bloomberg reported last week that Summers is already freezing Volcker out of many of his deliberations on economic policy. This sounds like the arrogant Summers who was fired as president of Harvard, not the chastened new Summers advertised at the time of his appointment. A team of rivals is not his thing.

Americans have had enough of such arrogance, whether in the public or private sectors, whether Democrat or Republican. Voters turned on Sarah Palin not just because of her manifest unfitness for office but because her claims of being a regular hockey mom were contradicted by her Evita shopping sprees. John McCain’s sanctification of Joe the Plumber (himself a tax delinquent) never could be squared with his inability to remember how many houses he owned. A graphic act of entitlement also stripped naked that faux populist John Edwards.

The public’s revulsion isn’t mindless class hatred. As Obama said on Wednesday of his fellow citizens: “We don’t disparage wealth. We don’t begrudge anybody for achieving success.” But we do know that the system has been fixed for too long. The gaping income inequality of the past decade — the top 1 percent of America’s earners received more than 20 percent of the total national income — has not been seen since the run-up to the Great Depression.

This is why “Slumdog Millionaire,” which pits a hard-working young man in Mumbai against a corrupt nexus of money and privilege, has become America’s movie of the year. As Robert Reich, the former Clinton labor secretary, wrote after Daschle’s fall, Americans “resent people who appear to be living high off a system dominated by insiders with the right connections.”

The neo-Hoover Republicans in Congress, who think government can put Americans back to work with corporate tax cuts but without any “spending,” are tone deaf to this rage. Obama is not. It’s a good thing he’s getting out of Washington this week to barnstorm the country about the crisis at hand. Once back home, he’s got to make certain that the insiders in his own White House know who’s the boss.

The Sanctity of AIG’s Contracts March 16, 2009

Posted by rogerhollander in Criminal Justice, Economic Crisis, Torture.Tags: AIG, aig bonuses, aig executives, chrysler, cia interrogations, contract concessions, contracts, Federal Reserve, ford, geithner, general motors, glenn greenwald, International law, Larry Summers, obama administration, roger hollander, treasury department, uaw, united auto workers

add a comment

Published on Monday, March 16, 2009 by Salon.com

by Glenn Greenwald

Larry Summers, Sunday, on AIG’s payment of executive bonuses:

Associated Press, February 18, 2009:

Apparently, the supreme sanctity of employment contracts applies only to some types of employees but not others. Either way, the Obama administration’s claim that nothing could be done about the AIG bonuses because AIG has solid, sacred contractual commitments to pay them is, for so many reasons, absurd on its face.

As any lawyer knows, there are few things more common – or easier — than finding legal arguments that call into question the meaning and validity of contracts. Every day, commercial courts are filled with litigations between parties to seemingly clear-cut agreements. Particularly in circumstances as extreme as these, there are a litany of arguments and legal strategies that any lawyer would immediately recognize to bestow AIG with leverage either to be able to avoid these sleazy payments or force substantial concessions.

Since the contracts are secret and we’re apparently just supposed to rely on the claims of AIG and Treasury Department lawyers, it’s impossible to identify these arguments specifically. But there are almost certainly viable claims to be asserted that the contracts were induced via fraud or that the bonus-demanding executives themselves violated their contracts. Independently, it’s inconceivable that there aren’t substantial counterclaims that AIG could assert against any executives suing to obtain these bonuses, a threat which, by itself, provides substantial leverage to compel meaningful concessions. Many of these executives were, after all, the very ones responsible for the cataclysmic losses.

The only way a company like AIG throws up its hands from the start and announces that there is simply nothing to be done is if they are eager to make these payments. One might expect AIG to do so — they haven’t exactly proven themselves to be paragons of business ethics — but the fact that Obama officials are also insisting that nothing can be done (even while symbolically and pointlessly pretending to join in the populist outrage over these publicly-funded “retention payments”) is what is most notable here.

Legal strategies aside, just as a business matter, one of the first things which every compnay in severe distress does is go to its creditors, explain that it cannot make the required payments, and force re-negotiations of the terms. That’s as basic as it gets. To see how that works, just look at what GM and other automakers did with their union contracts – what they were forced by the Government to do as a condition for their bailout. Obviously, if a company goes into bankruptcy, then contracts to pay executive bonuses are immediately nullified, but the threat of bankruptcy or serious financial distress is, for obvious reasons, very compelling leverage to force substantial concessions. And the idea that, in this economy, AIG executives (of all people) will be able simply to leave and go seek employment elsewhere unless they receive their “retention bonuses” (even assuming that’s an undesirable outcome) is nothing short of ludicrous.